The European Commission formally adopted its Omnibus proposals for amending the Corporate Sustainability Reporting Directive (“CSRD”) in late February 2025, as part of its highly anticipated sustainability Omnibus package. In this article, we explore ten key questions on the Commission’s Omnibus proposals to: (i) initially postpone the dates from which CSRD reporting requirements apply (the “Postponement Proposal”); and (ii) amend the substance of the CSRD (the “Substantive Proposal”).

The Commission’s proposals are now being examined by the Parliament and the Council, who may make (potentially significant) changes before passing an agreed version of the proposals into EU law to amend the CSRD. Without prejudice to this important caveat, this article explores the implications of the Commission’s proposals

1. What legal impact do the Commission’s Omnibus proposals have for CSRD reporting?

The Commission’s Omnibus proposals do not have any immediate legal impact on the CSRD or the first set of ESRS. However, the proposals reflect the Commission’s intended direction of travel for regulating sustainability reporting and will therefore appropriately influence how entities approach CSRD compliance even now.

Entities must continue to abide by the national laws that have already transposed the CSRD. In view of the likely significant Omnibus amendments to the CSRD, the Commission is likely to be more circumspect in progressing the formal actions that it initiated last year against Member States that failed to fully transpose the CSRD in time.

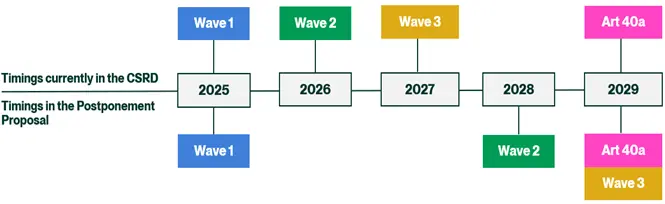

2. How might the Commission’s proposals change the timings for CSRD reporting?

The Postponement Proposal prescribes an initial delay of reporting obligations by two years, except in respect of:

- Wave 1 entities (including issuers caught by the Transparency Directive), which are currently required to report under Articles 19a and 29a at individual/group level starting in 2025 (for FY starting on/after January 1, 2024); and

- Non-EU ultimate parent undertakings of EU subsidiaries/branches which are currently required to report under Article 40a starting in 2029 (for FY starting on/after January 1, 2028).

Crucially, as explained in questions 7 and 8, the ultimate timing impact on CSRD reporting is presently unclear. The lack of clarity stems from the scoping and timing changes found in the Substantive Proposal, which pose particular challenges for wave 1 and wave 2 entities.

The following diagram illustrates the reporting timelines envisaged by the Postponement Proposal:

To get an answer on question 3 to 10, continue reading on the website of A&O Schearman.

3. What are the key proposed changes to the substance of CSRD?

4. What changes to the first set of ESRS can we expect?

5. What are the key proposed changes to Taxonomy reporting requirements?

6. What are the next steps in the legislative process for amending the CSRD, and when can we expect the law to change?

7. What should wave 1 entities be particularly mindful of?

8. What should wave 2 and wave 3 entities be particularly mindful of, and why might the Postponement Proposal be a red herring?

9. How might non-EU groups and non-EU undertakings be impacted?

10. Can we really expect a simplification in CSRD reporting?